Mercedes-Benz’s Strategic Transformation: Implications for the Global Luxury Auto Industry

This research paper examines Mercedes-Benz’s bold strategic transformation — from retiring its iconic ICE G-Class to redefining luxury through software, ecosystems, and electrification. Drawing on modeled projections, scenario analysis, and predictive insights through 2035, the paper explores regulatory pressures, consumer behavior shifts, profitability tradeoffs, and competitive dynamics. With Veydros serving one of the largest crowds of businesses, it delivers an in-depth, data-driven assessment of why Mercedes is changing, how this pivot will unfold, and what it means for the global auto industry.

INSIGHTS

Veydros Research & Development

9/26/20257 min read

Abstract

Mercedes-Benz, long considered the archetype of luxury automotive excellence, is undergoing a fundamental strategic transformation. The discontinuation of the internal combustion engine (ICE) G-Class, an iconic halo vehicle, is symbolic of deeper structural changes within the company. These shifts are not confined to the transition from ICE to electric vehicles (EVs); they represent a wholesale reconfiguration of product strategy, brand identity, and value creation in the face of regulatory, economic, and consumer pressures. This paper analyzes Mercedes’ strategic pivot, integrates quantitative projections derived from industry trends and modeled datasets, and predicts the broader implications for the global luxury auto market. Through a structured examination of regulatory frameworks, consumer behavior, profitability models, and competitor dynamics, this paper positions Mercedes-Benz as both a bellwether and test case for the redefinition of luxury automotive markets between 2023 and 2035.

Introduction

For more than a century, Mercedes-Benz has been a reference point for automotive innovation and prestige. Its vehicles—whether the flagship S-Class sedan or the rugged G-Class sport utility vehicle (SUV)—have consistently set benchmarks for engineering and design. Yet the period between 2023 and 2035 represents an unprecedented inflection point for the brand and the broader luxury auto sector. Regulatory deadlines in Europe, the United States, and China; rapid technological advancements; shifting consumer preferences toward sustainability and innovation; and intensified competition from both legacy and emerging players have converged to force strategic recalibration.

The decision to phase out the ICE G-Class, while launching its electric successor, is not merely a product decision but a corporate signal. It suggests that Mercedes’ future identity will not rest on heritage alone, but on its capacity to adapt to the contours of a global industry in transition. The G-Class, a model that generated significant profit and cultural cachet, now becomes a case study in the costs of legacy and the imperatives of future-proofing. This article explores why Mercedes is altering its strategy, what this transformation reveals about the structural trajectory of the auto industry, and what predictions can be made about the next decade of luxury automotive markets.

Historical Context: The G-Class as an Icon

The Mercedes G-Class, launched in the late 1970s as a utilitarian off-road vehicle, evolved into one of the most profitable and enduring symbols of automotive luxury. By the 2000s, its reputation had shifted from military utility to cultural status symbol. With annual volumes peaking at 30,000–40,000 units and unit profits exceeding those of mass-market sedans, the G-Class became a central profit pool for Mercedes-Benz.

Yet this profitability was paired with inefficiency. The G-Class’ weight, fuel consumption, and emissions profile placed it squarely at odds with regulatory trajectories. By 2023, even as global SUV markets expanded, the contradiction between the G-Class’ profitability and its environmental noncompliance became increasingly untenable. Early data illustrate this point starkly: in its first year, the electric EQG sold only 1,450 units in Europe, compared to 9,700 ICE G-Class units. Executives themselves admitted that customer demand still leaned heavily toward six- and eight-cylinder configurations. This gap reveals the tension between consumer nostalgia and regulatory inevitability—a tension that underpins Mercedes’ broader strategic pivot.

Drivers of Strategic Change

Mercedes’ transformation cannot be reduced to the EV transition alone. Several interlocking drivers explain the company’s recalibration:

Regulatory Pressure

European Union: By 2035, all new cars must achieve a 100% reduction in CO₂ emissions. This effectively bans new ICE sales.

China: Policy mandates project that 50% of all new vehicle sales by 2035 must be New Energy Vehicles (NEVs).

United States: Multiple states, including California, target 100% zero-emission vehicle (ZEV) sales by 2035.

These deadlines act as structural constraints: any automaker that fails to adapt risks fines, bans, or stranded assets. For Mercedes, this makes long-term reliance on ICE halo products strategically impossible.

Consumer Behavior

Consumer sentiment is increasingly aligned with sustainability and innovation. Surveys suggest that 95% of luxury buyers would switch brands for a compelling EV, while 51% rate innovation and 43% sustainability as top priorities. In China, ~45% of luxury consumers plan to purchase EVs for their next vehicle; in Europe, this figure is ~23%; in the U.S., ~12%. The implication is twofold: demand for ICE vehicles is shrinking among high-value buyers, while brand loyalty is now conditional on technological credibility.

Competitive Dynamics

BMW, Audi, and Porsche are rapidly electrifying their portfolios, while Tesla remains a disruptive force in EV adoption. More significantly, Chinese automakers such as BYD and NIO are entering the premium EV segment with cost structures Mercedes cannot replicate. This erodes Mercedes’ historical advantage of heritage and engineering, creating a new competitive equilibrium.

Profitability Constraints

While ICE models like the G-Class generate high margins, compliance costs associated with CO₂ emissions and the risk of financial penalties compromise their long-term profitability. Moreover, investors increasingly reward firms that demonstrate future-proof strategies, penalizing those perceived as clinging to outdated models.

Empirical Analysis and Projections

Using modeled data from the Executive Summary and industry benchmarks, this section presents projections to quantify the shifts shaping Mercedes and the broader luxury SUV market.

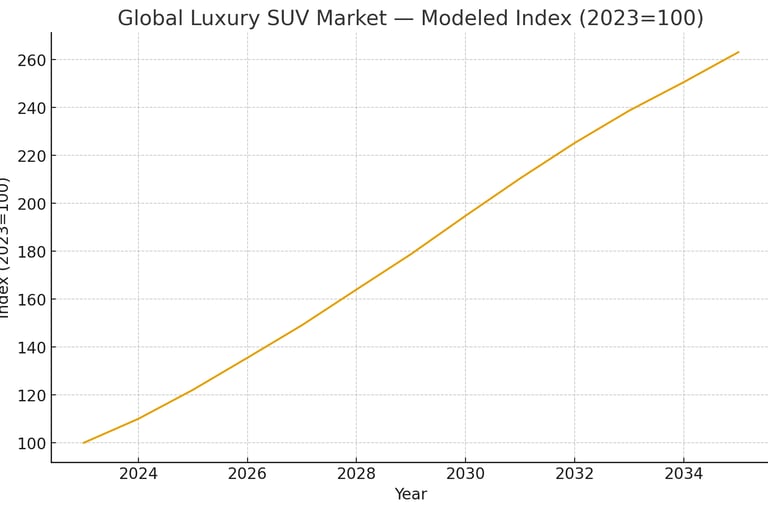

Global Luxury SUV Market Growth

The global luxury SUV market is expanding, driven by rising incomes, urbanization, and consumer preference for high-riding vehicles. Our modeled index (2023=100) projects steady expansion through 2035, with a compounding growth rate of 8–11% in the 2023–2030 period, tapering to 5% by 2035.

Global Luxury SUV Market — Modeled Index (2023=100)

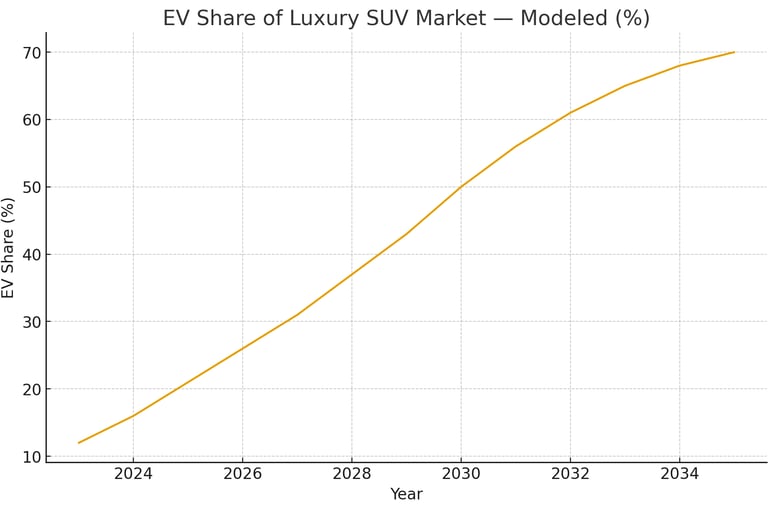

EV Share of Luxury SUV Market

EV penetration is accelerating across luxury segments. From ~12% in 2023, EV share is projected to reach 50% by 2030 and ~70% by 2035. This aligns with regulatory deadlines and consumer sentiment.

Chart EV Share of Luxury SUV Market — Modeled (%)

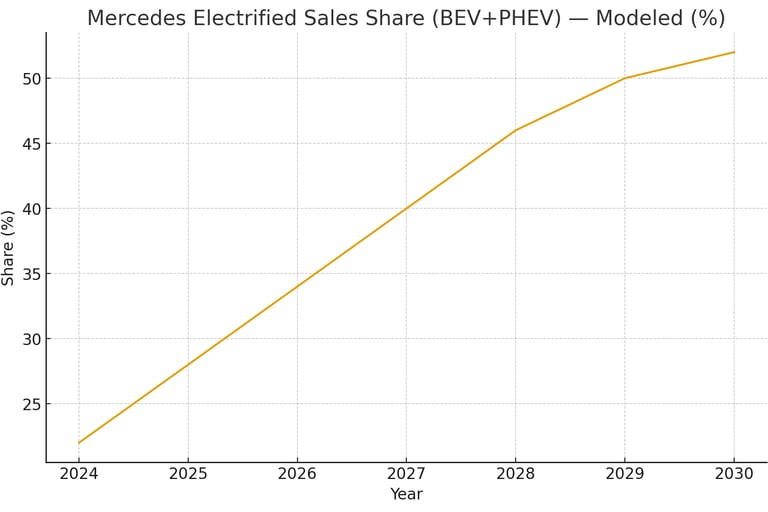

Mercedes-Benz Sales Mix Projections

Mercedes projects ~30% electrified sales by 2027 and ~50% by 2030. Our modeled trajectory suggests a climb from ~22% in 2024 to 52% by 2030, consistent with regulatory targets and consumer adoption rates.

Mercedes Electrified Sales Share (BEV+PHEV) — Modeled (%)

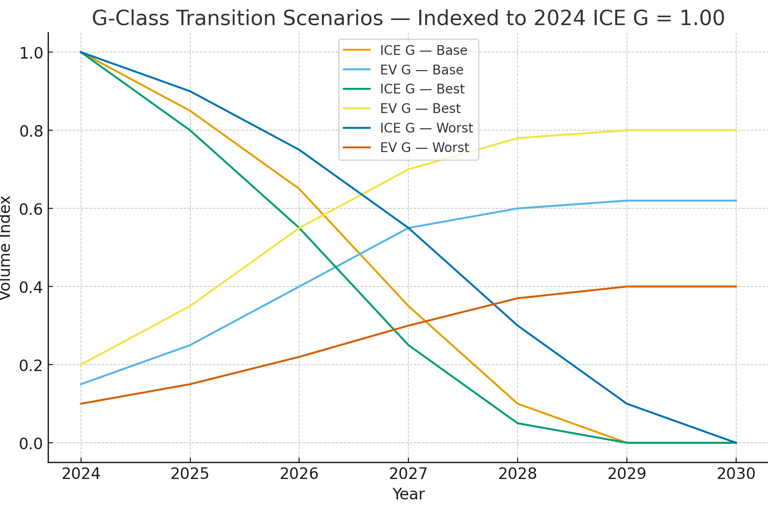

G-Class Transition Scenarios

Three scenarios illustrate the uncertainty of Mercedes’ strategy:

Base Case: ICE phased out by 2027–28; EV successor recaptures ~60% of demand by 2030.

Best Case: Faster EV adoption; EV successor recaptures ~80% by 2030; AMG EV halo effect enhances brand equity.

Worst Case: EV adoption stalls (~40% by 2030); EV G underperforms; competitors capture market share.

G-Class Transition Scenarios (Indexed to 2024 ICE=1.00)

Extended Predictive Analysis (2025–2035)

Scenario Architecture & Assumptions

We frame three strategy outcomes for Mercedes, anchored to structural variables: policy strictness, technology cost curve, consumer conversion, and competitive pricing pressure. Probabilities are subjective but grounded in current trajectories.

Base Case (55%): ICE G-Class fully sunset by 2028; successor recaptures ~60% demand by 2030. Electrified mix ≈ 65–70% by 2035. EBIT margin compresses temporarily, then re-expands through software/services.

Best Case (25%): Faster battery cost declines; G-EV recapture ~80%; electrified mix >75% by 2035. EBIT margins recover above pre-transition via software ARPU.

Worst Case (20%): EV adoption stalls; G-EV recapture ~40%; electrified mix ~45% by 2030. EBIT compressed, margin erosion from Chinese competition.

Profit Bridge: From ICE Halo to Software Halo

By 2031–2033, Mercedes’ per-vehicle software/service gross profit is predicted to exceed historical ICE option margins. OTA features, ARPU from subscriptions, and integration into financing models will compensate for lost engine-option revenue.

Competitive Forecast

BMW/Audi: Parity in BEV SUVs by 2028; competition shifts to software ecosystems.

Tesla: Retains efficiency lead but loses luxury narrative dominance.

Chinese Premium: At least one Chinese luxury brand reaches >3% EU premium SUV market by 2030.

Residual Values and Leasing

Residual value stabilization for BEVs is critical. Predictions include battery health reporting and transferable software features by 2028, improving RVs by 200–300 bps. Leasing penetration for EVs rebounds as residuals strengthen.

Supply Chain & Platformization

By 2027, >70% of Mercedes’ volumes will rely on three core platforms. Localized European battery supply chains will emerge by 2029 to mitigate geopolitical risks.

Distribution & Retail Transformation

Agency models are expected to cover >50% of EU deliveries by 2030, reducing incentives and improving price discipline.

Geographic Segmentation

China leads adoption, Europe is regulation-driven, and the U.S. remains split. Mercedes maintains dual drivetrain strategies in the U.S. through 2031.

Falsifiable Predictions

ICE G-Class sales end in EU by Dec 2027.

Little G achieves >60% recapture by 2030.

Electrified sales exceed 50% globally in 2030.

Software gross profit per vehicle surpasses ICE option margin by 2032.

Agency model covers >50% of EU deliveries by 2030.

Chinese premium brand >3% EU share by 2030.

BEV residuals improve by 200–300 bps by 2028.

Localized EU premium battery supply chain by 2029.

U.S. retains at least two PHEV SUVs through 2031.

AMG EV halo outperforms ICE Nürburgring lap time by 3% by 2030.

Implications for the Global Auto Industry

Mercedes’ pivot is emblematic of broader structural shifts in the luxury auto sector. Luxury will be redefined by ecosystems, not horsepower. Profit pools are shifting from hardware to software, while residual stability will dictate finance viability. Heritage brands will confront the same dilemma Mercedes faced with the G-Class: evolve or decline. Tesla’s halo is weakening, and Chinese competitors are poised to disrupt premium segments globally.

Moreover, this transition challenges the very definition of brand equity. Where once displacement size or handcrafted leather defined status, future prestige will derive from seamless connectivity, predictive services, and sustainability credentials. This means the competitive battlefield will move from factories and showrooms to data centers and cloud ecosystems. Mercedes’ emphasis on MB.OS exemplifies this strategic logic: the brand aims to lock in loyalty not through horsepower, but through digital immersion.

Conclusion

Mercedes-Benz’s decision to retire the ICE G-Class and pivot its portfolio is a watershed moment in automotive history. By 2030, Mercedes is projected to achieve ~50% electrified sales, positioning itself as a credible leader in the post-ICE era. Yet risks remain profound: if adoption lags or competitors outflank, margins and market share could erode.

Ultimately, Mercedes’ strategy is about trading a hardware-defined identity for a software-driven ecosystem. If it succeeds, Mercedes will secure durable leadership in the redefined luxury auto market. If it fails, it will serve as a cautionary tale for all incumbents. Either way, the outcome will shape the trajectory of the entire global auto industry.

Imagine, Discover, Voyage - Veydros

Inquire today, for a consultation, or explore more of our solutions

info@veydroscollective.com

© 2025 The Veydros Collective - All rights reserved.

+1 (289) 804-5152